Currently, the environment and water quality are at the forefront of New Zealanders minds. There is a general consensus that our environment is suffering from the strain modern society has put on it. As a consequence of this, the agriculture industry is coming under increased pressure and scrutiny to find solutions to address this problem. The subject has become a political football, with every one with a vested interest having their say, whether their opinions are informed or not.

The National Policy Statement for Freshwater Management places regulatory obligations on Regional Councils to improve or maintain water quality (MFE, 2016). Regional Councils around the country are in various stages of implementing policies to try to mitigate these problems. In Canterbury, Environment Canterbury is achieving this with the help and guidance of Zone Committees and catchment groups. The inclusion of local stakeholders and community engagement to help address local problems is a positive step. The outcomes locals decide will be far better received than policies imposed from outside influences.

To look deeper into the problem, I have studied the potential impacts of some of the proposed recommendations in the OTOP (Orari-Temuka-Opihi-Pareora) zone, one of the ten sub-regions in Canterbury. These Recommendations have been taken from the OTOP Draft ZIPA (Zone Implementation Program Addendum), which was released in December 2017 (OTOP Zone Committee, 2017). At the time of writing this document the above plan is in the submission period.

The specific part of the proposed plan I have looked at refers to the Rangitata-Orton area of the OTOP zone, which has been found to have high nitrates concentrations in ground water. The recommendations are that farms in the zone may have to reduce nitrogen leaching to ground water by up to 30-40% if water quality in the catchment does not improve in the next 5-10 years.

To test the implications of these proposed recommendations I have modelled a dairy farm, McClelland Dairies, which is situated in this zone. The purpose of the study is to determine what service industries will be significantly impacted from the implementation of such policies.

I believe this study is important because little information is circulated about who bears the brunt of cut backs to primary industries, whether these primary industries facing cutbacks are Agriculture, Mining, Forestry, or the likes.

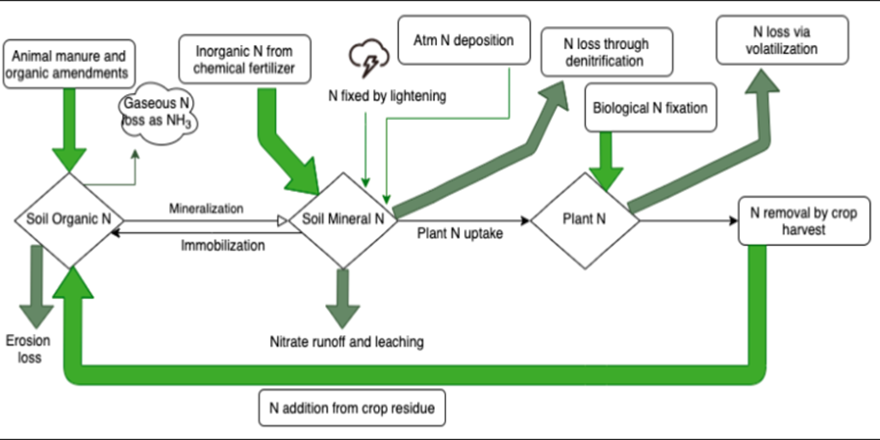

To investigate the problem, I created Overseer nutrient budgets for McClelland Dairies, using current farm management factors (stocking rates, inputs and outputs), to calculate the total amount of nitrogen being lost (i.e. leached) below the root zone from the whole property. The current nitrogen losses to water per hectare from McClelland Dairies, at Good Management Practice (GMP), are 108kg/N/ha/yr. Therefore, to meet the 40% reduction in nitrogen leaching losses, nitrogen loss has to decrease to 65kg/N/ha/yr.

I applied nitrogen mitigations to McClelland Dairies by implementing soil moisture monitoring, reducing imported supplementary feed and the stocking rate, to achieve the desired 40% cut in nitrogen leaching. Following this, I created financial budgets of the two farming systems (base farm (status-quo) and 40% mitigation scenario) and compared their financial performance, in order to determine the financial implications of the 40% nitrogen leaching reduction. This data created a picture of where the impact will be felt.

When I started out on this project, I expected that the nitrogen mitigation would have a significant adverse impact on farm profitability. However, some of the results came as a surprise. The difference in profit between the base farm and 40% mitigation scenario was relatively small. The base farm had a profit of $684,647 compared to the farm with lower nitrogen leaching which had a profit of $664,642. The difference was $20,005 or 2.9%.

The greater financial impact was felt in the businesses that supplied the farm. The farm with the applied mitigations and lower nitrogen losses had farm working expenses of $95,339 less than the base farm. This money would have been spent locally and had a direct impact to the local economy. The most significantly impacted service industries were feed suppliers, fertiliser companies, transport firms and local jobs across the service industries. All of these have flow-on effects to the greater economy.

With the issues highlighted in this study I recommend that there should be greater emphasis on investigating all the implications of placing restrictions on primary industries.

Personally, the environment is also important to me. I live, work and play in the same environment that we farm. I believe there is a balance to be reached between the impact that we as a society have on the environment and the financial viability of this same society.

We are already here so with the help of new ideas, science and technology and time, I am positive a solution to the problems we face will be found.