kellogg

AGMARDT supports leadership development with new Kellogg Scholarships.

AGMARDT Trustees have approved support for three new scholarships that seek to improve access to leadership development. The New Zealand Rural Leadership Trust (Rural Leaders) deliver the Kellogg Rural Leadership Programme, a critical point on the rural leadership pathway.

AGMARDT’s support will manifest as three scholarships specifically for the Kellogg Programme.

“We want to help improve access to leadership development by countering some of the challenges scholars can face. These may include the ability to meet the financial commitment required to undertake learning.

It is vital industry does all it can to ensure leadership potential is given the space it needs to grow. To help achieve this, we’re thrilled to give our support to scholars looking to enter the Kellogg Programme,” said Lee-Ann Marsh, AGMARDT General Manager.

How the AGMARDT Leaders Scholarship works.

The AGMARDT Leaders Scholarship allows three scholars to enter the Kellogg Programme per year. It covers the $6,500 fee for the Programme. A fee already generously subsidised by Rural Leaders’ Investing Partners, including AGMARDT.

Applicants for the AGMARDT Leaders Scholarship are encouraged to contact the Programmes Manager at Rural Leaders to discuss the opportunity and how it might be best tailored to their own circumstances.

“We are grateful to AGMARDT for their continued support of leadership development in the Food and Fibre Sector. Their support reflects AGMARDT Trustees’ desire to make leadership development as accessible as possible, especially those who might not have the balance sheet support of bigger organisations.

This also recognises that in a fast-changing environment, we need grounded leaders who are strategically capable, now more than ever,” said Chris Parsons, Rural Leaders CEO.

The new AGMARDT Leaders Scholarship will be available from Kellogg Programme One, January 2023, and joins three regionally available Scholarships that also support participation in the Kellogg Rural Leadership Programme.

These are:

AGAMRDT Leaders Scholarship

Three scholarships to participate on the Kellogg Programme per year valued at up to $6,600 each. These scholarships seek to increase access to leadership development.

Whanganui and Partners Regional Scholarship

Two scholarships per year to promote leadership in the Whanganui Region. Valued at $2,500 each, the scholarships are available to those attending NZ Rural Leaders Programmes who are from the Whanganui region or contributing to the Whanganui region.

Te Puni Kōkiri Scholarships

Up to two scholarship places on the Kellogg Rural Leadership Programme may be awarded. Valued at $6500 each, the Te Puni Kōriri Scholarships support Māori in the Food and Fibre Sector to develop stronger strategic leadership skills.

Whāngarei A&P Society Scholarship

One scholarship per year to cover fees. The Whāngarei A&P Scholarship aims to grow future strategic leaders for Northland’s Food and Fibre Sector.

Dame Jenny Shipley: On Leadership. On Point.

On leadership. On point.

Lynsey Stratford has discovered farmers make a few assumptions that aren’t very helpful – like accepting the fact that work might be dangerous and there’s nothing anyone can do about it. As Lynsey explains, “There are changes we can make, but those assumptions and those mindsets have been deeply held for quite some time.”

As a consultant, Lynsey helps the primary sector with people management and development services and training. And, when it comes to health and safety she says, “We shouldn’t expect people to just know this stuff, but rather teach them and support them as they develop skills.”

Lynsey’s research report unpacks the paradox that while farmers care about their people, farms as workplaces are overrepresented in fatal accident and injury statistics. So, what can be done to improve this?

Bryan Gibson, editor of Farmers Weekly.

I’m Bryan Gibson, Farmers Weekly Editor. This week, I have a very special guest, Dame Jenny Shipley. How’s it going?

Dame Jenny Shipley, 1984 Kellogg Scholar, Bay of Islands.

Very well, thank you.

Bryan: Good. And where are you calling in from today?

Dame Jenny: Well, I live in Russell in the Bay of Islands now. And while I still do a lot of traveling domestically and when I can internationally, this is where we call home.

Bryan: Oh, wonderful. The winterless north.

Dame Jenny: The winterless north, and it couldn’t be a greater contrast really, from my beautiful Canterbury electorate. But even learning to garden in the north is an entirely different process. But I’m enjoying it very much.

Bryan: Now, you grew up down in the Deep South, is that right? And spent a lot of your political career at least, in Mid–Canterbury?

Strong South Island roots.

Dame Jenny: Yes, I was born in Gore and my father was a Presbyterian Minister in Pukerau at the time. So many of those early roots were in a truly rural area. And interestingly, I’m going back there this weekend to take part in a nice ceremony. So I stay connected with a lot of those old roots, even though I’m now living somewhere else.

I spent a lot of my time in the South Island, and the early part of my life, in Nelson and that also has transformed. I don’t think there was a grapevine in Blenheim, or in the Marlborough area when I was a child. It’s a magnificent example of intense of horticulture today.

As a student I went to Canterbury and met Burton and the rest is history. We farmed and then I went into politics and had the great privilege of representing one of the most productive electorates in the country in that central and Mid-Canterbury area.

Bryan: Such a powerhouse of a rural area isn’t it?

Dame Jenny: Very much, yes.

Kellogg and the desire to lead.

Bryan: You connected with Rural Leaders for the first time doing a Kellogg Scholarship back in the early eighties, is that correct?

Dame Jenny: Yes. We were young and farming, and I was already involved in a lot of community leadership. At that time the challenges for agriculture in New Zealand were huge. The change was immense, the economic viability was demanding, interest rates were horrifying. Rural communities were very active, with a lot of emphasis on leadership.

I got given the opportunity to apply for the Kellogg Rural Leadership Programme, which was an emerging force at that stage. I forget whether it was year three or four that I was a member of – but it was a fabulous experience and in many respects it clarified my desire to lead.

The Programme taught me a lot about what else I needed to focus on in order to be effective. But it definitely gave me the strength and sense of impetus to get on – initially as a Counsellor in my local Malvern area and then into politics.

Is sector history repeating?

Bryan: We talk about the early to mid-eighties in the farming world. It was obviously, as you say, such a disruptive time. Many people think that we’re going through a similar sort of thing now. Do you see those comparisons?

Dame Jenny: Well, I think the commodity cycle is much stronger at the moment, although it’s clearly able to be volatile depending on what happens both at home and abroad.

The other difference, I think, is that agriculture today in New Zealand is not dependent on government subsidies. At that stage you’ll recall, there were multiple transitions going on – the support for agriculture was being removed, the markets were extremely volatile and the farming community was really facing challenges on multiple fronts.

Even in my early years as a Member of Parliament, the residual effects of that period flowed through – it was a very difficult period. Today I think that while there are huge challenges coming up economically, I personally think the agricultural sector is in a very resilient state.

But what is different now, is that there are so many regulatory pressures coming on farming which I don’t think were present in our era. And so, yes, there are huge challenges, but I think the economic viability overall gives at least some ability for farmers to confront those. I think the leadership question is different too, though, and perhaps that’s something that needs to change. So it’s relevant for where we are now.

Bryan: How is that, do you think?

Dame Jenny: Well, when we were farming, all of us belonged to Federated Farmers. It was a widespread group. Husbands and wives turned up and it was an active process in most local communities. I’m not familiar with whether that’s the case now. But like many organisations, I think that they’ve become more professional.

But whether the grassroots element of representation is as strong, I don’t have such a feel for that. But I think that what we’re coming into is that we have to have both the agricultural leaders reflecting the experience of farmers on the ground and making the case very clearly about what can and can’t be done, and indeed what has been done.

We need to share our good news more often.

If I can just pause on this point for a moment. I’ve observed enormous change by farming in response to public pressures. I travel quite a lot around the country and have just have been down through the Waikato – right into the West Coast part of it.

One of the things that struck me over the last five years is that what started off as tree planting on agricultural land for emissions purposes, now the work around wetlands and the fencing of streams and things. New Zealanders can be very confident that the farming community is not only responding but leading in some of these areas.

To come back to the point, I think that for farming to advocate for itself, it’s not only advocating for what’s annoying and frustrating them, but there’s also a huge need for us as an agriculturally strong community to continue to share both the gains and the commitment of the agricultural community to farming well both for themselves, the community, and the future. I think that’s a big change.

When we were farming, many were just farming to survive. Now, I see farmers all over the place investing not only in best practice for themselves, but I do see a lot of change. I think the voice of that needs to be shared across the community much more broadly so that the urban New Zealand population both values agriculture and understands that it’s moving in response to many of the concerns that urban communities have.

Bryan: Farming, as you say, is always evolving for the most part in New Zealand because we are very good at it, and improving. That gets lost sometimes.

Dame Jenny: Well a lot of it is a social response. I mean, farmers will tell you that they are fencing streams and planting for their own benefit and the benefit of their own environment. But there’s a huge public good element in it which unless people either have a chance to see, or you share how much is being done, or see the change that’s going on.

A sector supporting New Zealand through tough times.

I think that urban-rural split has always been a risk in New Zealand and it’s one we can’t afford to give airtime too. Because, frankly, if you just thought that even in the COVID period, if we had not had a strong agricultural sector during the last three years when the global economy had been disrupted, New Zealand’s position economically would be far more dire than it is at the moment.

Tourism collapsed, a number of other productive areas were compromised and yet agriculture was able to carry a huge proportion of the earnings, as it’s always done. But thankfully, on a strong commodity cycle at this particular time, and again, I think we should name the value of agricultural exports. The effort agriculture puts into the New Zealand economy to support our way of life, in a broad, holistic sense – not a them and us sense.

We’re in this together, being the best we can be at home and selling the best we can abroad in a best practice sense. I think if we keep sharing that over and over again, there’ll be a better understanding between rural and urban communities.

Leadership needs to reflect the people on the ground.

Bryan: Just touching on what you mentioned earlier about how historically, people like Federated Farmers, organisations like that, had a very, kind of a, grassroots focus. It’s quite evident at the moment around the emissions pricing process that a large number of those grassroots farmers think that the farming leadership has, if not deserted them, then certainly not represented them well. What’s your take on how they go about that? And what are the challenges that those farming leaders have in engaging with the government on things like this?

Dame Jenny: Well look, I’d be the last one to criticise them because I know how hard it is. I have admired the agricultural leadership, that they have taken a more inclusive, let’s find solutions together approach. I have been involved in a number of significant working parties not only on emissions, but in a number of areas that I can think of which I’ve simply been a distant observer. But I’ve noticed that level of engagement.

The problem is, in any leadership model, if you aren’t both working with, and then reflecting the people on the ground who actually live agriculture every day and have to implement the stuff, not only physically but also economically, then you have to test whether your leadership is in isolation as opposed to being able to carry people forward.

I do think we have to support the leadership group because unless they are able to foot it with the officials and the government ministers and be supported at that level, then they’re clearly not serving their constituency anyway. But every organisation, and I don’t want to make a judgment on Federated Farmers because I simply am not close enough to it, but there have to be systems where it’s not only consultation.

Often we say, well, we consulted, or we sent out a document and gave them a chance to comment. I think that for people to genuinely become supporters of a regime, they have to have a deep sense of ownership. They need to be able to see themselves in whatever is proposed as opposed to seeing something being imposed on them, which they don’t or can’t relate to.

So the test of high quality engagement and consultation has got to be that measure of – can the people we’re representing see themselves in the proposed solutions or are we just saying, well, regardless of what you think, you’ve got to be there in five or ten years’ time. That’s not easy to do. I think in New Zealand’s circumstances, whether it’s agriculture or Maori – Pakeha relations, or any of the other demanding spaces, we’ve just got to put the time and work into it.

The power of industry at the highest level of decision-making.

Bryan: Now, just digging into that a little more. I mean, you were obviously in central government for a long time. What’s it like in those meetings with industry? How much power do the industry leaders from the agricultural community have when they sit down around the table with the likes of MPs, Prime Ministers, officials?

Dame Jenny: The answer is, it depends. And I’m thinking back on two or three occasions where the agricultural sector and governments were working intensely. When a government decides, for example, to break up monopolies, I think the conversations are quite demanding.

I recall at the time that we decided to break up a number of public organisations, the electricity sector and of course the dairy industry was in the line of sight. That was never an easy conversation and the agricultural leaders, and particularly the directors of the original company very much resisted that. In those moments, you’ve got to put the economic argument of why these particular sectors needed to be able to face competition, not only in their growers interest, but also in New Zealand’s market in the world. The resilience and flexibility to attract investment.

We were trying to grow the New Zealand economy and grow the efficiency of the New Zealand economy in the world. So to some extent, in those big strategic moments, it’s tense, because sometimes you’ll have agricultural leaders with you as champions. Sometimes you’ll have small players wanting you to act and take on the big players.

So there’s many dynamics going on.

Usually before those moments, if it’s a strategic question, the ministers will have debated the relative merits of this before they go barging in and say, well, look, the government has decided to strategically move forward and create competition in the agricultural marketing sector, or whatever it is. And then you try and engage.

It’s a wee bit like the emissions environment where you’re having to say, look, we have to work out a way in which to change. It is going to be different from what is the case now, so let’s try and work out where the mechanisms are and how we can move forward.

Sometimes you’re responding to requests from the agricultural sector to solve problems and then it’s straightforward. Your meet as equals at the table. You put the facts on the table, you get the officials to work through and come up with a solution. Often in the majority of cases, things just get sorted out. But in the big, complex policy issues, where big change is required, there’s higher degrees of tension, but generally you get there in time.

The Kellogg Programme and leadership pathways.

Bryan: Now, you mentioned to me before we came on that as well as the Kellogg Programme, you’ve been involved in a number of other leadership programmes. Do you think there are good pathways into leadership positions in New Zealand at the moment?

Dame Jenny: The Kellogg Programme is fantastic. I’d encourage any community to keep identifying young leaders and to promote them into those Programmes. Often people think, these people are too young. I must have been, I don’t know, 32 or thereabouts when I went into Kellogg. Often at that stage, you haven’t identified your leadership purpose and your particular intentions as to how you will use your leadership skills. But others often see leadership potential in those young people.

There’s no question that our political environment, our economic and social environment, need younger people coming through all the time in order for us to be able to shape the future successfully. I would encourage people to look for those chances and look for individuals who they can sponsor or promote and make sure they support them. Because often these are the young people, male and female, who have got kids and are trying to run a farm and all that. So the programmes themselves are a big commitment, but it’s worth it.

Supporting leadership development.

The other programme, I was actually involved in establishing, was Rural Women Stepping Out, I think we called it at the beginning. It was run out of Lincoln and was only initially a two or three day – and sometimes only a one day programme.

But it was at a time where there was huge economic stress on many farming communities. Lots of women came and had lots of examples of how women entrepreneurs were establishing small rural businesses to supplement the income of farms at that time.

Much of it was in the cottage industries, or services – many aspects of agriculture. I think that sharing and bringing together helped a lot of those women sustain the pressure of that period. I guess my point here is, rural communities are very important to New Zealand and keeping both men and women well and supporting them to be as engaged as they can be, both in running the farms and running the rural communities of which they’re a part.

Any support in leadership and leadership development is well worth the investment. So whether it’s the leaders at universities or the sponsors that are the companies who make these things happen, so that these families can make the choice, I think agriculture and New Zealand benefit from programmes like Rural Women, the Kellogg Programme and the Field Scholarships. All of those platforms are invaluable in terms of the legacy and the investment that they’ve made.

Bryan: Thanks for listening to Ideas That Grow. This podcast was presented by Farmers Weekly. For more information on Rural Leaders, the Nuffield New Zealand Farming Scholarships or the Kellogg Rural Leadership Programme, please visit ruralleaders.co.nz

Katie Vickers: Banking on a sustainable future.

Ideas That Grow: Katie Vickers: Banking on a sustainable future.

Lynsey Stratford has discovered farmers make a few assumptions that aren’t very helpful – like accepting the fact that work might be dangerous and there’s nothing anyone can do about it. As Lynsey explains, “There are changes we can make, but those assumptions and those mindsets have been deeply held for quite some time.”

As a consultant, Lynsey helps the primary sector with people management and development services and training. And, when it comes to health and safety she says, “We shouldn’t expect people to just know this stuff, but rather teach them and support them as they develop skills.”

Lynsey’s research report unpacks the paradox that while farmers care about their people, farms as workplaces are overrepresented in fatal accident and injury statistics. So, what can be done to improve this?

Bryan Gibson – Editor of Farmer’s Weekly.

I’m Bryan Gibson, the Farmers weekly editor. This week, I’m with Katie Vickers. How’s it going?

Katie Vickers – 2019 Kellogg Scholar.

Good, Bryan.

Bryan: And where are you calling in from?

Katie: I’m ringing in from Fairlie today.

Bryan: And that’s where you call home at the moment?

Katie: Yes. Recently moved down here from Christchurch. So getting back into the rural life. But loving it.

Bryan: And you are currently working for Rabobank as a Sustainability Manager, is that right?

Supporting producers through changing times.

Katie: Yes, I am. My role is around helping to support the banks sustainability ambitions and supporting our clients, in what is a reasonably challenging environment out there – just helping and supporting them, understanding what changes are coming and how that will impact their businesses and I guess wrapping our arms around them and helping them through that.

Bryan: You’re right, there’s a lot of stuff going on in that space that farmers have to deal with. So it’s kind of cool that the banks are arm in arm with them facing up to that challenge, isn’t it?

Katie: Yes. And I guess the changes are pretty complex, but we probably need to start thinking slightly differently around how we tackle some of those challenges.

One of the reasons I wanted to work for a bank was that you can see that they’ve got quite a strong lead in terms of how they can support clients. I guess at Rabobank we’re committed to the agri-sector and I love that kind of passion they’ve got for the sector.

Our role is around how we support them, but also how we link them up with the right knowledge and networks. Because it’s such a complex topic and so different for every farming system. So it’s important for us to be able to understand their unique needs and make sure that we’ve got the right toolkit to support them in making good decisions for their business.

Researching food nutrients on Kellogg Programme.

Bryan: Have you always worked in the agri-food sector or is it something you’ve evolved into over time?

Katie: No, I’ve always been in the agri-sector. I grew up on a sheep and beef farm just north of Kaikoura, went to Lincoln University and then decided after Lincoln, that I definitely wanted to stay in the agri-sector.

So I managed to land a job at Farmland’s Cooperative, and I worked there for eight years. About six of those years was actually in marketing, so I’ve come from a marketing and comms background and then spent my last two years there in a sustainability role. Then just recently moved to the bank, so it’s been an awesome journey.

Bryan: Now, while that was going on, you applied yourself to the Kellogg Programme, and you took a look at nutrients in food. Is that correct?

Producing food to positively impact human and the planet’s health.

Katie: Yes. So my topic was around putting the food back into food. The question I was looking to answer was what would it take for our primary industry to produce nutrient dense food? I think the reason why I wanted to explore that was I’ve always been brought up with a really holistic approach. I care deeply about the health of our planet and health of our people.

I’ve got a twin sister who is a holistic health practitioner, so she works on the how do we help people’s health, because we’ve got a massive crisis in that space.

So my passion has always been, what role does agriculture have to play in that? How do we work with our soils better to influence the food that we eat, which in turn influences the health of our people? It’s a massive topic. It was hard to even scratch the surface on a lot of that stuff.

I did a lot of interviews and research with soil scientists, nutritionists and industry leaders, and I got some really cool insights out of that. No real answers, but lots of different things to consider.

Bryan: People would think the food that New Zealand food producers make is nutrient dense and natural and grass fed and all that sort of thing already. So is there more that can be done at the farm level to enhance that?

Kellogg research and the impact of soil on the food we produce.

Katie: I’m not an expert in this space and I will never claim to be, but my thinking was really expanded when I read Nicole Masters’ book – For the Love of Soil. She talks about the relationship that we have with the soil. In this day and age, there’s so much more we’re learning about the soil and the microbiology of the soil, and the knowledge we have of that is growing.

As we understand more, we need to do more on-farm. So the role that my research played was understanding that today we use a lot of synthetic fertiliser, and we have quite a strong reliance on that, and that hasn’t been a terrible thing, but moving forward, how do we understand how to use our soils better so we don’t need to have such a reliance on some of those synthetic inputs coming into our farm systems.

I you look at the kind of environment we’re in today with the rising input costs, it’s about how do we create more resilient farming systems, and having a different lens on what that might look like in the future. So the research I did was, okay, how do we understand our soil more to understand the impact it has on the food that we produce?

Bryan: And what sort of insights did you get from some of the people you interviewed?

The shift to quality over quantity and premium pricing.

Katie: One of the really interesting ones I did, I didn’t actually interview him, but I did a whole lot of research on the work that Dan Kittredge has done out of the States. He’s got a business called The BioNutrient Food Association.

His role is looking at some tools consumers could use in the future to be able to scan Apple A and Apple B as an example and see the different nutrient composition of those apples and therefore make a decision as to why they might be paying $2 more for Apple A because it’s got a higher nutrient profile.

Those tools aren’t in market and in bulk yet, but I have absolutely no doubt they will be in the future. So that’s the kind of thing could change the landscape of farming, when consumers have got the power in their wallet to be able to make those decisions, to say, well, you know, I want to know why I’m paying more for this apple, because I’m getting the nutrients that I need. With that, you’re hoping there’s been less environmental degradation to produce that product, whether that be apples or meat or whatever.

Bryan: Yes, I guess that sort of thinking has become more prevalent with the pandemic, with people really thinking a lot about what they eat and keeping their base level health as high as it can be. So it’s really top of mind for a lot of people.

A food system under stress.

Katie: For sure. I think it’s pretty obvious our food system is under stress. And whether it’s talking about a climate crisis, a human health crisis or health crisis, a biodiversity collapse, there’s all these different things that play in to each other. One of the key points I like to think about is that we don’t want to look at these things in isolation.

If you look at the human health crisis we’ve got, and even the latest pandemic, these pieces have a real interconnectedness and it’s quite a different way to think about it.

I think the more that we think about the connection between the crisis of our planet and the crisis of our human health at the moment, it might help us to think differently around how we handle these things in the future.

Bryan: That sort of thinking ticks a few boxes at once, as you say. It can do more for people’s health – and a focus on soil can also do more in terms of freshwater quality and in terms of greenhouse gas emissions and biodiversity. All sorts of things do come together as one.

A lot of people, when you talk about, say, regenerative agriculture or related fields, a farmer might say, well, I’ve yet to see the value-add for me. So if I’m going to reduce production to adopt these things, I need to make that up somewhere else.

So how does a sustainability manager at Rabobank approach these things?

Planting seeds – one conversation at time.

Katie: That’s a great question. I guess my personal mission is to just plant little seeds in people’s minds around how they think about these things. I guess I’ve always believed that you’ve just got to approach it conversation by conversation and people will take different things from the conversations that they have with you.

My role at the bank, is to just support and understanding and what role Rabobank needs to play in this space and how we support our clients. That’s going to look different for every client we have.

We have some clients that are in the regenerative space and really loving it and seeing benefits. We’ve got others that will want to be exploring it and others are saying, that’s not for me – there’s no right or wrong, it’s just how do we help create resilient farming systems in the future and make sure that people are profitable, sustainable and enjoying the life they lead. Because at the end of the day, if they’re not doing that, there’s not a huge amount of value in it.

So I guess my role is just to have these conversations and I see business having a really important role in influencing the way we think. And as a young leader, I guess we can help create the future and it’s important that we are part of that. I want to be part of creating that future.

Katie Vickers, Kellogger, Rabobank Sustainability Manager.

Bryan: I guess Rabobank being a global, agriculturally focused bank would have a sort of a long term view and a strategy around where things are going and what needs to be done to continue to do business in this space. So that would feed into a lot of the work that you’re doing?

Katie: Yeah. We are lucky to have that global aspect. I guess it’s one of the pros of working for such an awesome business because we’ve got all these insights from across the globe to help our thinking. But I definitely reckon New Zealand is leading the way, particularly in the climate space and understanding at a farm systems level, what we’re dealing with.

Bryan: Yeah, it is. And another thing I guess we need to remember is that it’s not just a value proposition, it’s increasingly become a cost of entry and market access, isn’t it?

Katie: Yeah. I was late with that because I’m not a technical expert, but I come from a marketing background but when you have tricky conversations with people who might not agree with some of the changes that are happening, or are struggling to comprehend it, which I totally empathise with.

One of the pieces I always lead with is the market. We export 90% of what we produce here in New Zealand. So whether we like it or not, what’s happening, what consumers are demanding and what the market is saying, is really important to how we respond. So we have to understand those market signals to make sure we’re producing what’s going to be valuable and what’s needed from our customers.

Bryan: Yes, I used to work a little bit in PR as well, (we used) the old adage, if you’re explaining, you’re losing, quite often. It’s got to be obvious and it’s got to be transparent. You’ve got to front foot these things, otherwise someone will front foot it for you.

Katie: Exactly.

Bryan: So what made you apply to the Kellogg Programme in the first place?

Kellogg, equipping today’s leaders for tomorrow’s challenges.

Katie: It was part of my development plan when I was at Farmlands, and I am eternally grateful for the opportunity to do the Programme. It was such an important time … the Programme really helped to widen my thinking around what influence business could have in helping to solve some of the challenges I could see coming in the agriculture sector. Having the opportunity to do that was just incredible.

I know that I probably wouldn’t be where I am today if I hadn’t had the opportunity to do that Programme. I guess it was the people we were exposed to and the time that was carved out to really explore some of the ideas that came up – that was the really valuable stuff for me.

Bryan: I’ve been to one or two of those Kellogg alumni conferences, and just the feeling in the room is quite different to a lot of places. You know what I mean? There’s such a good sort of camaraderie between the alumni of the Programme.

Staying connected with the Kellogg network.

Katie: Yes. I think for me, I’m a people person, so the connections with people in the industry were just phenomenal. Even now, if I really want to talk to X, Y or Z to find some information and you said you did Kellogg, people are so willing to talk to you. I guess it just gives you the opportunity to speak to people who will challenge your thinking.

As I’ve grown up and matured, I love having that. I love having people who will challenge my own thinking because it helps deepen my knowledge and my thoughts. Being able to have the opportunity or the exposure to speak to different people and have different perspectives is just so invaluable.

Bryan: Thanks for listening to Ideas That Grow, a Rural Leaders Podcast in partnership with Massey and Lincoln University AgMardt and FoodHQ.

Kellogg Rural Scholar Series: ‘Dairy Insights’.

Here’s an introduction from Rural Leaders CEO Chris Parsons, on the new Dairy Insights report.

New Zealand’s food and fibre sector is full of capable, and purpose driven people. Supported by DairyNZ, Livestock Improvement Corporation and an incredible group of partners, the New Zealand Rural Leadership Trust is privileged to be entrusted with growing many of these people in their leadership journey.

A key aspect of the rural leadership approach is research-based scholarship. The clarity of thought and confidence this approach promotes is transformative.

The set of reports précised in this edition are penned by Scholars from the Kellogg Rural Leadership Programme. The Kellogg programme has been equipping rural leaders for strategic impact since 1970. The selection of reports is just a sample of reports by Scholars from the Dairy Industry.

They grapple with the big issues facing New Zealand Dairy and are written by people living and working in the Sector. Many Kellogg and Nuffield Scholars go on to live their research. They build businesses. They advance community and social enterprises. They influence policy and advocate for animal and environmental outcomes, informed by an ability for critical analysis and their own research-fuelled passion. Rural Scholarship is about impact.

In the following pages we are pleased to précis 14 dairy research reports by Kellogg Scholars. The full reports can be found at https://ruralleaders.co.nz/kellogg-our-insights

The reports traverse topics as wide and timely as innovation, markets, people, sustainability and social issues.

Ngā mihi,

Chris Parsons

and the NZ Rural Leaders Team

Download and read the full report here:

More issues from the seriess

Kellogg Phase Two – what does it look like?

One of the highlights of the Kellogg Rural Leadership Programme is the Wellington based, Phase Two. Scholars of the 48th Kellogg Programme (internally referred to as K48), will begin their Phase Two in September.

The week is delivered in a specific order designed to reveal the political and economic context carefully, each step building on the last.

Dr Scott Champion, will facilitate, expertly introducing Scholars to this part of the Programme. Phil Morrison facilitates on other Kellogg Programmes. Dr Champion deftly fills the spaces between influential speakers, encouraging discussion and imparting his own extensive knowledge, so that the whole experience is as seamless as it is inspiring.

So, what will Phase Two look like for the Scholars of the 48th Kellogg Rural Leadership programme?

Note, this gives an idea of how any Phase Two will flow. Details and speakers are subject to change.

Kellogg Phase Two - The Political and Economic Context for Leadership.

Day One

Dr Champion introduces this phase.

Lian Butcher talks about the role of local and regional government. Lian is General Manager, Greater Wellington Environment Group.

Jessica Smith is a Kellogg Scholar and talks about Māori governance and management, as well as her role as Regional Director of Te Tai Hauāuru.

Vangelis Vitalis talks about trade policy and market access.

Mike Petersen discussion session. Mike wears and has worn many hats, one of which was as SATE, New Zealand’s Special Agricultural Trade Envoy.

He is passionately committed to advancing New Zealand here and on the global stage.

Day Two

Dr Champion leads each morning with a reflection session, designed to discuss the previous day, draw insights, and connect these with the upcoming speakers.

Chris Parsons, CEO Rural Leaders will talk Civics (the rights and duties of citizenship) to get the morning underway.

Nicola Hill and Rachel Groves, cover political structures and processes. Nicola is Te Whanau a Apanui Takutai Moana Application Lead and was formerly nearly five years with the department of the Prime Minister and Cabinet. Rachel is a Principal Policy Analyst with the Ministry of Justice.

Barbara Kuriger, a Member of Parliament for the National party, gives some insights into the inner workings of government.

Hon. Damien O’Connor, MP for West Coast-Tasman, Minister of Agriculture, Minister for Trade and Export Growth, Biosecurity, Land Information, and Rural Communities.

Question time, followed by networking at PWC.

Day Three

Reflection session.

Ewan Kelsall and Kevin Hackwell, speak about the role of NGO’s, interest groups and lobbyists. Ewan is a Senior Environmental Policy Advisor for Federated Farmers and Kevin is Group Manager Campaigns and Advocacy for Forest and Bird.

Sam Halstead, speaks about the role of journalism and PR. Sam is Director at Latitude, Strategy and Communication.

Leaders Meetings. Small groups have one-on-ones with Sector leaders. This is a no-holds-barred discussion where leaders share their good decisions, their bad ones and what they would do differently if they could.

Networking function at PWC. The programme dials up the networking during phase two with this opportunity to get in front of industry leaders and policymakers.

Day Four

Reflection session.

Anna Rathe, Submissions Workshop 1 and 2. In two parts and delivered either side of lunch, Anna leads this workshop. Anna is a Strategy and Risk Policy Leader with Horticulture New Zealand.

Sam Halstead, Communications Skills Workshop. Also delivered in two parts, this workshop expertly covers a lot of ground, focusing on the pieces that matter.

Day Five.

Reflection session.

Martin Workman, Chief Advisor at the Ministry for the Environment. Martin leads a ‘big issues’ discussion and talk.

Project Workshop. This 90-minute session is designed to help develop project topics. It’s a good time to air any challenges Scholars might be facing.

Goal setting and Phase Two close.

Want to experience this for yourself. Register your interest in the Kellogg Rural Leadership Programme today.

2023’s January and June intakes at Lincoln.

Kellogg Programme One, Lincoln: 24 January – 7 July 2023

Applications close: Sunday, 30 October 2022.

Kellogg Programme Two, Lincoln: 13 June – 30 November 2023

Applications close: Sunday, 16 April 2023.

The carbon credit currency

By Sam Mander, Environmental Consultant, The AgriBusiness Group and 2022 Kellogg Scholar.

The article is reprinted from the Real Estate Magazine, with permission from the publisher The Real Estate Institute of New Zealand.

Indigenous forest land and the carbon sequestration opportunity for New Zealand landowners always seems to be downplayed — deemed too expensive, too hard, or inferior compared to exotic forests.

Sam Mander, Environmental Consultant at The AgriBusiness Group, debunks this myth and provides an understanding of how to identify the indigenous carbon opportunity.

Kanuka, manuka, regenerating native vegetation or planted native restoration sites hold a significant opportunity for carbon sequestration. But fundamentally, where the opportunity really lies in this space is where a natural seed source is present.

Land with naturally regenerating indigenous forest requires no capital input, eliminating the usual barriers of expensive planting regimes and delicate forest management.

We don’t want to discourage the planting of new native areas, particularly around areas of ecological significance, but to capitalise on the low hanging fruit, landowners must take advantage of existing native seed stocks and develop these areas to accelerate the growth of regenerating New Zealand’s indigenous landscape.

Determining eligible indigenous forest land

Indigenous forest areas are eligible to enter the Emissions Trading Scheme (ETS) if they meet the Ministry for Primary Industries (MPI) forest land definition.

What is carbon sequestration?

Carbon sequestration is the process by which carbon dioxide is absorbed during photosynthesis, and is stored as carbon in biomass (trunks, branches, foliage, and roots). Source: nzfoa.org.nz

MPI’s forest land definition states that forests must:

- Reach at least one hectare in area

- Reach at least 30 metres average width

- Have species that can grow five metres high

- Have the potential to reach 30% canopy cover

- Meet the above as of 1 January 1990 or after

- Have met all of the above as of 1 January 1990.

If a landowner has property that has manuka, kanuka, mixed podocarps, or areas they are thinking of planting native species (including in riparian zones — the interface between land and a river or stream) carbon credits can be earned if the areas meet the forest land definition.

One carbon credit is equivalent to one tonne of carbon sequestered; therefore, the tonnes of carbon sequestered by the forest each year are the total number of annual carbon credits available.

Tonnes of carbon are calculated on a per hectare basis, and the value of one tonne is equal to the current carbon price ($76/NZU/tonne).

You’re typically looking for a natural seed source present with conditions that favour natural dispersion, growth and succession. Any native species can be included if it has the potential to reach five metres in height at maturity.

The most common example of opportunity is regenerating kanuka and manuka forest land areas.

To earn carbon credits, landowners need to electronically map the land to certain standards and capture aerial imagery to prove the forest area meets the forest land definition.

The value of credits a landowner can receive and for how long they will receive them largely depends on the species growing on the land.

The MPI carbon lookup tables determine that indigenous forests can earn carbon credits from sequestration in the first 50 years of growth.

How to assess the native forest area

This can be a difficult process for landowners; fortunately, professional forestry companies and environmental consultants like myself have developed methods for assessing forest land definition and providing the result of the assessment to MPI for a successful ETS application.

“The value of credits a landowner can receive and length of time they will receive them largely depends on the species growing on the land.”

Depending on the forest scenario, we use a combination of ground vegetation sampling, plotting, and integrated drone imagery to determine and prove this. In most cases, this is where an expert may need to be involved.

A recent example is a property with an indigenous natural seed source. An assessment found it had 35 hectares of post-1989 indigenous forest land that had regenerated since 1990, with a forest age of approximately 17 years.

Forest species were predominantly kanuka, manuka, among other mixed podocarps. Carbon credits can be claimed for the remaining 33 years of carbon sequestration.

Economically speaking, at the current carbon price, this equated to an average annual cash flow of $16,000, or cumulatively, $539,000. In summary, the opportunity to earn carbon credits for indigenous forest land is significant, particularly where a natural seed source is present.

The property mentioned above is among many that we have worked on which provides a great example of the type of property that is common around rural New Zealand and one that holds value from indigenous carbon sequestration.

Planting trees to offset carbon isn’t a silver bullet against climate change.

However, carbon credits allow landowners to balance the scales for those unavoidable emissions on the path to reduction and has potential to generate financial benefits for those who wish to engage in these sustainable practices.

Download Sam’s report Carbon Sequestration Potential.

How Resilient Farmers Thrive In The Face Of Adversity

By Jack Cocks and Joanne R. Stevenson.

Article is reprinted from The Journal with permission from the publisher, NZ Institute of Primary Industry Management

Farmers face adversity from multiple sources and additional challenges to other sectors of society. To date, there does not appear to be a simple high-level resilience-focused model for how farmers can be more resilient ‘personally’.

This article, which is the result of a Kellogg Rural Leadership Study on ‘How Resilient Farmers Thrive in the Face of Adversity‘, is a first step towards developing that model.

The study found there were three key strategies that facilitated farmer resilience – purpose, connection and well-being.

Adversity affects farmers from multiple sources

Like all members of society, farmers face adversity in a range of forms from health crises to financial volatility, family challenges and personal loss. Due to the nature of their business, however, farmers are more vulnerable than those in other industries to climate challenges and global market shifts. They are also often toiling at the coalface of legislative changes and can have less access to appropriate support services.

More than other industries farmers have strong identity ties to their land and business, meaning that disruptions to the farm are de facto disruptions to the farming family. They also typically live at their place of work.

The current global environment (autumn 2022) – experiencing climate, a global pandemic and a war in Eastern Europe – highlights the dynamism, volatility and interconnected global marketplace in which New Zealand farmers operate.

Developing strategies to recover quickly from adversity, or ‘building resilience’, is essential to achieving long-term success in farming. While there are a number of tools and resources available that address social-emotional resilience, there does not appear to be a simple, high-level resilience-focused model developed specifically for farmers.

Such a model could be used by farmers when facing adversity to ask themselves, ‘Are we implementing the key strategies and techniques (both as an individual and as a team of individuals) that we need to be resilient in the face of this adversity?’

More than other industries farmers have strong identity ties to their land and business, meaning that disruptions to the farm are de facto disruptions to the farming family.

Context

The lead author, Jack Cocks, an Otago high country farmer, experienced adversity from a life-threatening brain injury which saw him in a coma, suffer a cardiac arrest, a seizure and a pulmonary oedema.

On day one in hospital Jack’s family was given a prognosis that their husband, dad and son would likely be dead today. The best case scenario was that he would survive but spend the rest of his life in an institution.

He obviously did survive, and the following six years saw him undergo 15 major surgeries and spend eight months in hospital re-learning to talk, and several times re-learning to walk.

Through this experience and recovery Jack has been told that he is a resilient character. He has been asked to give several talks to farmers on his experience and how he developed resilience through adversity.

He found that giving these talks was a humbling and surprising experience for the feedback received.

However, the presentations were based on just one farmer’s thoughts and he had two questions he could not answer from them:

- The adversity he had faced, while bad, was it any worse than what many people face?

- Were his ideas on resilience applicable to all farmers, or were they just the ideas of one farmer who had faced some adversity?

Five areas of adversity

The five areas of adversity and a brief synopsis of each case are given below:

Health

Doug, who farms on the East Coast, faced severe adversity in the form of depression. This was primarily brought about through farming in what became an eight-year drought.

Natural disasters, climate and weather

Andy, who farms in Canterbury, has farmed through a succession of major weather events, snowfalls and droughts. He has a great deal of knowledge about how to farm through adversity.

Financial

Kevin and Jody, who farm in Otago, have faced a very high amount of adversity in their lives starting from before they emigrated to New Zealand.

Their major adversity in this country has been financial, in the form of a very low dairy payout in their first two seasons as 50:50 sharemilkers.

Family

Brent and Jo, who farm in Southland, experienced a number of challenges to farm succession early in their farming career. Communication and a desire to split assets evenly among all children, farming and non-farming, were the major challenges.

They have since done everything right to complete succession with Brent’s siblings and are an example for how farm succession can successfully be completed with their own children.

Personal loss

Melissa lost her husband to cancer and has since done tremendous good for her community.

It would be impossible and unfair to compare each of these stories. The level of adversity and the situations they have faced are so different that any of them would have responded differently, perhaps better, perhaps worse.

The choice of case study participants provides representation of the common sources of adversity farmers in New Zealand face and a cross-section of the likelihood of adversity from the ‘wow, that is incredible’, to ‘yes, our neighbours have been in that situation – I’ve seen it many times.’

The most remarkable story of resilience is notable for the breadth of the sources of adversity and the severity of the situation they faced.

One of the case studies is therefore an important reminder of the possibility of compounding disruptions, where adverse events seem to stack up, showing the way that resilience can be repeatedly eroded and then built back up.

Jack was able to identify some of the case study participants because they have shared their stories publicly, mobilising the power of story-telling to process their own adverse event and improve the lives of others by sharing their message.

Interviewing and examining their stories collectively revealed common themes that underpinned this diverse range of experiences.

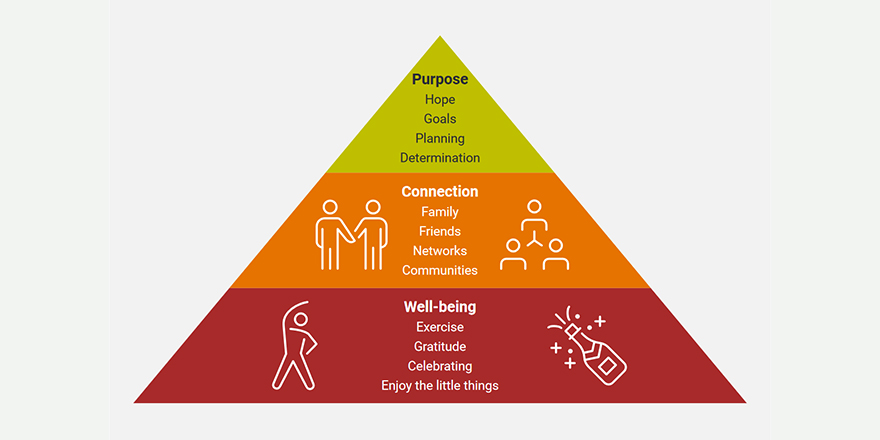

Resilience strategies and the ‘Resilience Triangle’

Analysing the interviews revealed the common resilience strategies that the five case study participants knowingly or unknowingly put in place in their lives.

These strategies are captured in the form of a three-level triangle, the ‘Resilience Triangle’:

Purpose

This is the reason we are doing what we’re doing; the ‘direction’ of the triangle, the ‘why’.

Connection

This is the middle of the triangle; the ‘glue’ that holds it together, or the ‘who’. This is keeping connected with other people – friends, family, farming networks and local communities.

These connections are the people in our lives who buoy us up and encourage us to achieve, to rise above, and to have courage when going through adversity.

Well-being

This is the base of the triangle. It is, ‘what do I need in my life to be well’ or to be happy and content? It is the ‘foundation’ for resilience, the ‘what’.

Participants in the study placed different weighting and had different consciousness of the use of these strategies, but they are common across all five cases.

Key to the effectiveness of these resilience building strategies is the combinations of approaches across the three levels and how the participants have implemented the strategies in their lives.

For each of these strategies there were four ‘enabling techniques’ below each one that the farmers used to enable resilience at each level.

There are different enablers that underpin their sense of purpose, connection and well-being. We could identify enablers that, when missing, eroded resilience at different levels of the triangle.

The lead author cites that after brain injury induced balance issues, having sufficient stability to be able to dress standing up was a cause for celebration after having to sit on the bed to do this for so long. Enjoying the little things such as seasonal foods, a sunrise, or the first birdsong in the early spring were all cited as enablers of well-being.

Conclusions

This study was concerned with developing a theory for how resilient farmers thrive in the face of adversity. It found that the case study participants employed three strategies in their lives to be resilient:

- they lived with ‘purpose’ in that they had a clear understanding of ‘why’ they were doing what they were doing

- they were very good at keeping ‘connected’ with those people around them who would and could help them through periods of adversity

- they also understood what they needed to do to keep ‘well’ – what they needed in their lives to be happy and content.

Also, for each of these three strategies there were four enabling techniques which these farmers employed to facilitate each strategy.

Rural professionals supporting our farmers need a clear understanding of not only the causes of adversity, but some of the strategies and techniques they can use to be resilient.

The future global environment in which New Zealand farmers operate will face significant volatility, turmoil and potentially subsequent adversity.

Rural professionals supporting our farmers need a clear understanding of not only the causes of adversity, but some of the strategies and techniques they can use to be resilient. We believe this study is a first step in crystallising how resilient farmers thrive in the face of adversity.

Acknowledgements

Thanks are due to the Kellogg Rural Leadership Programme for developing and delivering such an excellent programme. Also, to the five case study participants who have openly shared their stories of adversity and resilience, as they are remarkable and inspirational farmers.

Jack Cocks is a sheep and beef farmer in the Otago high country and previously a partner in AbacusBio, a Dunedin agribusiness and science consultancy. Dr Joanne R. Stevenson is a Principal Consultant with Resilient Organisations Ltd and farms in partnership with her husband on a North Canterbury sheep and beef property.

Corresponding author: jackcnz@icloud.com

Lincoln University, Kellogg, and Rural Leaders – a collaboration spanning decades

Based on campus since 1979, the Kellogg Rural Leadership Programme has a long connection with Lincoln University, having been developed by the Kellogg Company as a way of enhancing global leadership capability.

In 2013, the programme was transferred to the newly-formed New Zealand Rural Leadership Consortium, which merged it with the prestigious Nuffield New Zealand Farming Scholarship to create a single organisation. Four years later, the consortium became a registered charitable trust and changed its name to the New Zealand Rural Leadership Trust (Rural Leaders).

A partnership known as the Pāhautea Initiative was announced in late 2020 between Lincoln University, Massey University, the Agricultural and Marketing Research and Development Trust (AGMARDT) and Rural Leaders.

The initiative focuses on lifting education levels across the sector and building deeper leadership benches in the regions, with the aim of creating a sustainable future for food and fibre. Accreditation of core programmes is key to delivering on the partnership’s purpose.

Kellogg accreditation strengthens the bond with Lincoln University.

Rural Leaders, Lincoln University and Massey University have further strengthened ties by offering academic accreditation for those who undertake the Kellogg Rural Leadership Programme.

After completing the programme, Kellogg scholars can opt into a Postgraduate Certificate in Commerce.

Alternatively, they can allocate the 60 credits they can earn towards the 180 required credits for a Lincoln University taught master’s degree.

Scholars can also elect to use their 60 credits towards a master’s degree at Massey University.

Additionally, accreditation may soon be available for the Nuffield New Zealand Farming Scholarship, although this is a work in progress, says Rural Leaders’ Programme Manager Lisa Rogers.

“Theoretically, it would be a diploma, or 120 points towards a 180-point taught masters.”

A dedicated Kellogg programme team.

The Kellogg Rural Leadership Programme team – including Rural Leaders facilitators Dr Scott Champion and Phil Morrison, Dr Patrick Aldwell and examiner Professor Hamish Gow – work hard to provide a varied and stimulating learning experience.

The programme includes two papers, the first of which requires the completion of specific assignments and is delivered by Scott Champion and Phil Morrison.

The second paper, delivered by Dr Patrick Aldwell, involves completing a research project and giving a presentation at the end of the programme.

Rural Leaders deliver three Kellogg Programmes a year, with two based at Lincoln University. The other, in alignment with the Pāhautea Initiative’s aim of growing flourishing regions, is regionally based. The next location, in May 2022, will be Whanganui.

Each programme is delivered to 20 to 24 scholars. Numbers are kept low to ensure a transformative experience, as the Kellogg journey is as much about learning from fellow scholars and developing a pan-sector network of friends as being exposed to industry leaders and new ideas.

A shared history and a shared future.

Rural Leaders have a strong presence on campus and increasingly share alumni with the university now that Kellogg scholars can gain a Lincoln postgraduate certificate.

Lisa Rogers says she is keen to see the long association continue to grow.

“We often get graduates from the Lincoln Future Leaders Scholarship Programme coming through to do the Kellogg. While we may not see recent undergraduates apply, it’s something we see happening later in their careers.”

Fun fact: Up to 50% of participants in any one Kellogg Programme have previously graduated from Lincoln University.

The Mackenzie Study – a view of leadership

The Mackenzie Study – a view of leadership

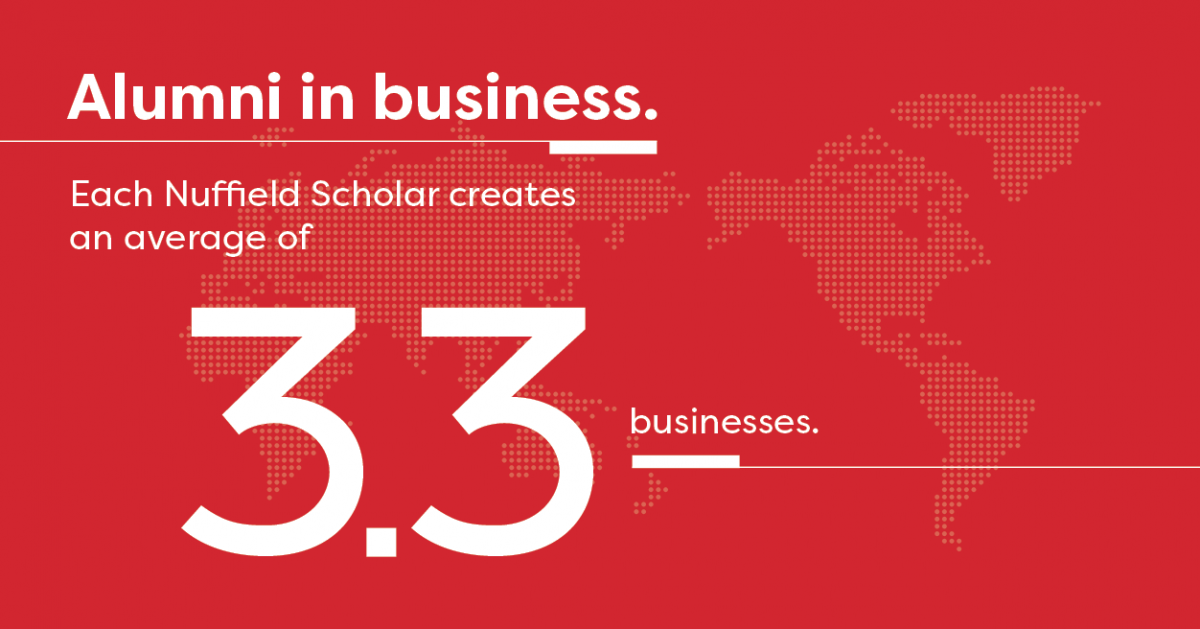

The Otago Business School and the Department of Economics recently conducted research on behalf of The Mackenzie Charitable Foundation and The New Zealand Rural Leadership Trust.

‘The Mackenzie Study’ revealed remarkable results on the personal gains in entrepreneurial skills attributable to participation in the Kellogg and Nuffield Programmes. It is Nuffield Scholars’ broad and consistent level of achievement over time, that resonates most.

Preliminary findings are a compelling case for anyone considering applying for a 2022 Nuffield Scholarship, or looking to develop their leadership ability through the Kellogg Rural Leadership Programme.

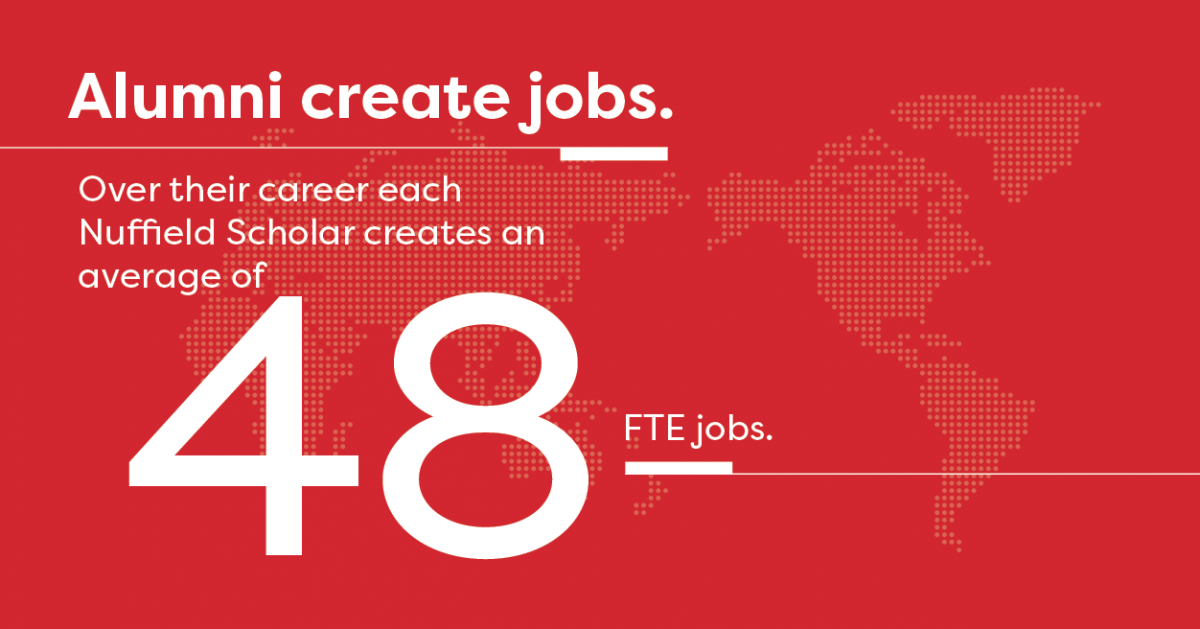

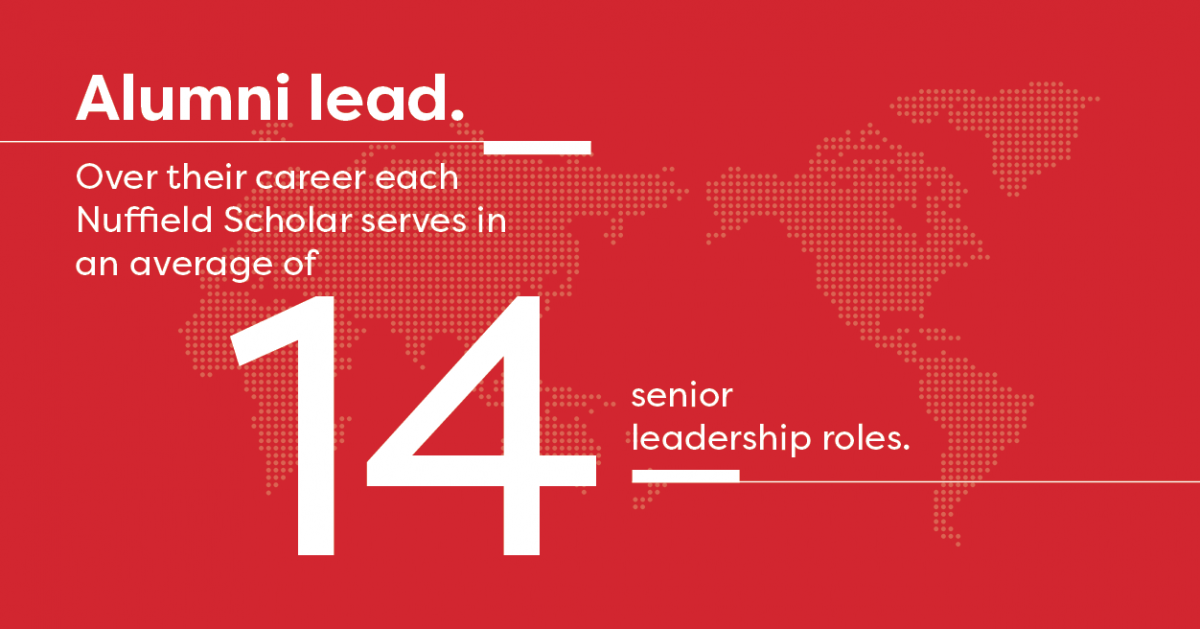

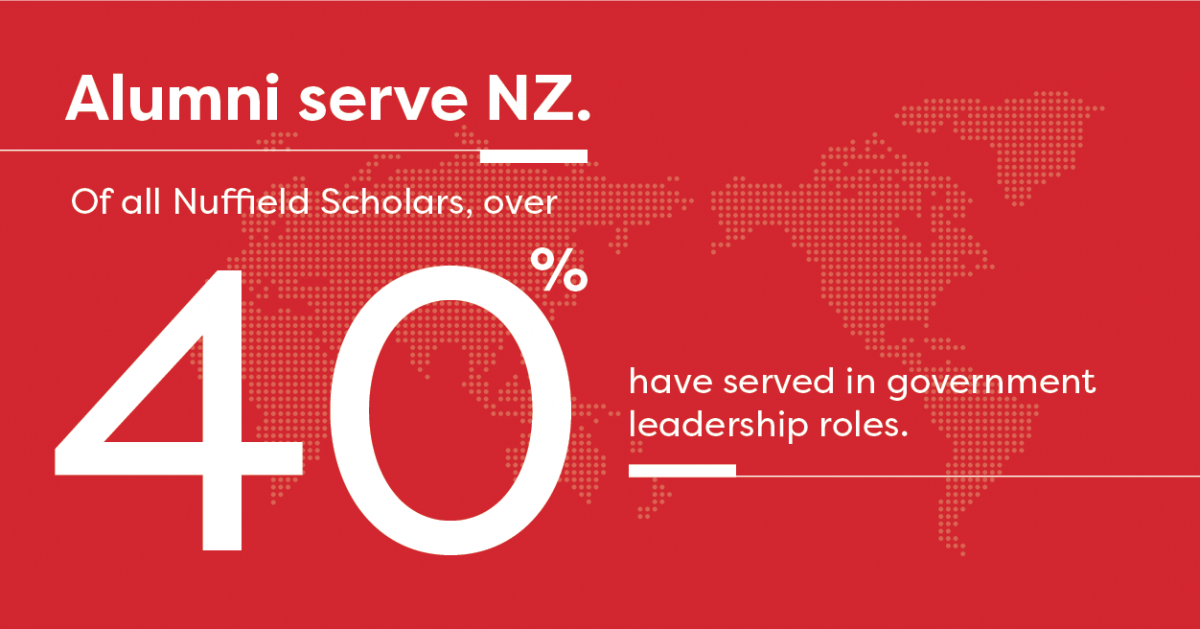

A comprehensive survey of Nuffield Scholarship Alumni was conducted in June this year, with invitations sent to all 135 living alumni.

The study had an unusually high participation rate of over 50%, especially given the flooding in Canterbury.

We’ll be presenting more results in due course, including comparisons between alumni and current cohorts. For now, here are just some of the findings demonstrating the professional accomplishments of Nuffield Scholarship Alumni.

Each result is a strong call to potential applicants for the 2022 Nuffield Scholarships, to apply before midnight this Sunday, August 15.

Kellogg Tai Tokerau Networking Event – 1st December 2020

Join us at the Kellogg Tai Tokerau Networking Event!

Tuesday, 1st December at 6.30pm

At the Orchard, 35 Walton St, Whangarei

Hear from our Northland Kelloggers – Paul Martin and Graeme Peter about their Kellogg experience. Network with other Kelloggers!

Explore how doing the Kellogg Rural Leadership Programme in Tai Tokerau in 2021 can help you accelerate your career in the Food and Fibre Sector.

Paul Martin, 2016 Kellogger

“The Kellogg programme has been a key part in my governance journey. I’ve developed a number of networks through the course. Those networks have supported me and inspired me to continue my growth both professionally and personally.”

Paul Martin

Paul is a self-employed Agribusiness Consultant working under the Headlands banner, with clients throughout the Northland region. In addition to his consultancy work Paul is involved in a number of governance roles within the Dairy Industry and Bee Industry. Locally, Paul is the President of the Whangarei Bee Club, and a Trustee of Reconnecting Northland.

Paul’s 2016 Kellogg research topic focused on ‘How New Zealand dairy farmers can thrive in the face of milk price volatility.’

Graeme Peter, 2020 Kellogger

“The connections and learnings I have gained from doing a Kellogg are incredible. I feel very privileged to be part of the course and in particular the calibre of my cohort.”

Graeme Peter

Graeme is the Regional Food Safety and Assurance Manager for Fonterra in Northland. He works with farmers in Northland on animal welfare, food safety and assurance claims on farm.

Graeme will graduate from the 2020 Kellogg Rural Leadership Programme at the end of November. His Kellogg research topic is ‘Corporate Social Responsibility of Aotearoa Dairy Farmers – the Current Situation and How We Win.’ This body of research focuses on the four pillars of corporate social responsibilities (economic, legal, ethical and philanthropic).

Graeme’s drive is to keep Aotearoa dairy farmers and their families as leaders on the world stage, in our farm systems and animal welfare. Graeme says “The Northland Dairy sector faces many challenges and my Kellogg project has helped me bring a wider New Zealand and international view to these issues and has also provided access to incredibly talented and informative people.”

Alice Rule: Sustainability at heart

Alice Rule, Kellogger and emerging young leader in sustainability, is researching the circular economy of glass in the New Zealand wine industry as part of her Kellogg research project. Through her work, she hopes to drive awareness about using glass made in New Zealand in the wine industry. Click here to find out more about Rule’s research project.

NUFFIELD AGRIBUSINESS SUMMIT – MARCH 23, 2020

After our fantastically successful one day Summit alumni event in 2017 we promised you another one in three years (based on your preferred frequency). We are pleased to announce that our next Kellogg alumni event has been confirmed for 23 March 2020.

What is even more exciting is that we are combining this event with the Nuffield2020 International Event, as part of a one day International Summit being held in Christchurch and hosted by Nuffield NZ. With a theme of Fast Forward – this is a day focused on future solutions showcasing new business models. There will be lots of discussion and debate with International and New Zealand speakers who are leaders in change and business solutions, that will inspire, provoke and challenge your thinking.

We know as Kelloggers you also love to reKonnect – so we are organising some alumni networking events around the Summit with the help of Canterbury Kellogg alumni including a cocktail function on Sunday evening. The details of other events will be announced shortly.

All we need you to do now is:

- Diary this date – 23 March 2020

- View the Summit Programme

- Get your Kellogg cohort together for a reunion

- Register now for the Summit and get in fast to secure your accommodation

- Follow the Social Shares below and keep up to date with what’s happening at the Summit

If you have questions about the Summit and associated Kellogg events feel free to contact us at programmes@ruralleaders.co.nz.

EXPERIENCE AN EVENT TO GROW | CONNECT | INSPIRE

Have your say on the proposed new freshwater rules

Make the most of the two-week submission extension for the proposed new freshwater rules.

Submissions will be accepted up until 31st October, so make sure you have your say.

For more information or resources visit www.beeflamb.co.nz, www.dairynz.co.nz or www.mfe.govt.nz

Social licence about trust

Penny Clark-Hall is passionate about helping rural communities.

Ms Clark-Hall is the founder of New Zealand’s first social licence consultancy, helping farmers and agri-businesses earn and maintain their social licence to operate.

She is excited about speaking at the Women’s Enviro Evening in Clinton later this month, saying meaningful change had to come from grassroots, or “the ground up”.

That had a domino effect and, if everyone did their “own little bit” then it all added up to something big, she said.

The evening, which will be held in the Clinton Town Hall on Tuesday, July 30, has been organised by local woman Sandra Campbell.

Mrs Campbell, who with husband Chris is in an equity partnership on a 500-cow dairy farm between Clinton and Balclutha, attended a food and fibre conference in Christchurch a few years ago.

She left feeling enthused both about their own business and also about sustainability. The aim was of this month’s meeting was to bring top speakers back to community level and make it accessible, she said.

Click here to read more.

It’s not weak to speak

It was a warm, sunny afternoon in Takaka in Golden Bay.

As daylight beamed through a window only to hit the back of a curtain, Kellogger, Wayne Langford found himself bedridden in a cool, dark room. He had been flat on his back every afternoon for more than a week to escape his constant mental anguish.

But this day was different.

“I had like an out-of-body experience.

“It was as though I was hovering above myself looking down and saying ‘what the hell are you doing in bed?’”

It was 2pm on March 18, 2017.

It was his 34th birthday.

“I couldn’t help but think I should be out and about celebrating with people, not stuck indoors….”

To read more about Wayne Langford by Luke Chivers, click here.

Calling all dairy farm workers

Blake Marshall from Ngai Tahu Farming is completing his Kellogg Rural Leadership project on “The importance of developing positive stress management and mindset skills in young dairy farmers”.

He is wanting to survey dairy farm workers.

If you are a dairy farm owner or employer and want to be involved in this survey or receive a copy of the report on completion, please email him on Blake.Marshall@ngaitahu.iwi.nz

Q&A conference call for aspiring Kelloggers

We are hosting three Q&A conference calls for anyone who is interested in completing a Kellogg Course. The calls are hosted by our General Manager Anne Hindson. We encourage you to attend even if you have no questions, this will help you gain a deeper understanding of what the programme is about.

Click here for the call details.

Reserve Bank Bulletin

This report, released today, covers the banking side of NZ Dairy Farming and makes for an interesting read. Recent Kellogg graduate Zach Mounsey alongside others, has helped analyse the findings, create and publish the report….

No bull behind record milking attempt

The record-setting exercise is the brain-child of healthy farming campaigner Ian Handcock who was responsible for the Farmstrong initiative, aimed to improve farmers’ mental and physical health. In 2013 Handcock’s Kellogg rural…

Giving back drives award winner

Jessie Chan-Dorman is a Kellogg Rural Leadership scholar, has completed a Fonterra governance programme and was the recipient of Canterbury’s Institute of Directors aspiring director award in 2014. And she was named 2017 Fonterra…

Young Farmers chief wins scholarship to attend Stanford Bootcamp

NZ Young Farmers chairman and recent Kellogg alumni Jason Te Brake will attend the Te Hono Movement Stanford Bootcamp in the United States after receiving the Emerging Primary Industries Scholarship.

Kellogg Alumni Hayden Peter won the emerging talent category

Excellence in New Zealand’s sheep industry was celebrated in Southland with the annual Beef and Lamb New Zealand Sheep Industry Awards.

No bull behind record milking attempt

“The record-setting exercise is the brain-child of healthy farming campaigner Ian Handcock who was responsible for the Farmstrong initiative, aimed to improve farmers’ mental and physical health.

In 2013 Handcock’s Kellogg rural leadership project on dairy farmer health highlighted how sedentary the job had become, and its effect on farmers’ fitness.”

https://farmersweekly.co.nz/section/dairy/view/no-bull-behind-record-milking-attempt